DUAL report: Cyber insurance market approaching inflection point as tolerance for further softening nears its limit

Summary

- DUAL’s analysis – Finding a Floor – shows that 2026 represents a critical juncture for cyber insurance as profitability comes

- Report outlines two possible paths: stabilisation supporting sustainability or continued softening risking a sharper correction

- Underwriting discipline and performance set to define the next phase of market development

The global cyber insurance market is approaching an inflection point, according to a new report from DUAL, which warns that sustained softening, rising exposures and an elevated threat landscape are converging to test the market’s long-term sustainability.

Cyber insurance continues to play a vital role in enabling resilience against an increasingly complex and interconnected threat landscape. With the global cyber insurance market approaching a significant inflection point, our DUAL team has developed a global outlook that brings together data driven trends and perspectives from our regional cyber experts

A market in transition

DUAL’s analysis indicates that 2026 will be a pivotal year, with signs that the market is nearing a “pricing floor” – particularly in the United States, which has traditionally been a bellwether for global trends.

Cyber insurance has moved rapidly through distinct phases: early exposure-led growth, a sharp pricing correction and, more recently, sustained softening. With pricing continuing to decline, exposures expanding and the cyber threat landscape remaining elevated, profitability is being eroded gradually. Without a shift in underwriting discipline, further softening risks a more severe correction.

DUAL’s analysis of pricing trends reveals a pronounced bifurcation across territories, with the US – accounting for around 70% of global cyber gross written premium and historically the first mover in underlying performance and pricing trends – providing the clearest signal on the likely direction of travel.

The lion’s share of global softening is currently being driven by international markets, where conditions remain favourable for buyers. Average pricing in these markets has fallen by 43% since 4Q23, according to DUAL’s research, reflecting a still-strong underwriting performance for most carriers.

*Source: DUAL analysis based on publicly available market and proprietary data

Margins under pressure amid elevated risk

Underlying cyber risk remains high. Increasing claims severity, broader policy coverage and growing supply chain exposures are creating a more complex underwriting environment. At the same time, intensified competition is leading to lower pricing, larger line sizes and looser terms, resulting in more risk being underwritten for less premium. These dynamics are contributing to margin compression across all major regions.

Regional divergence and shared trajectory

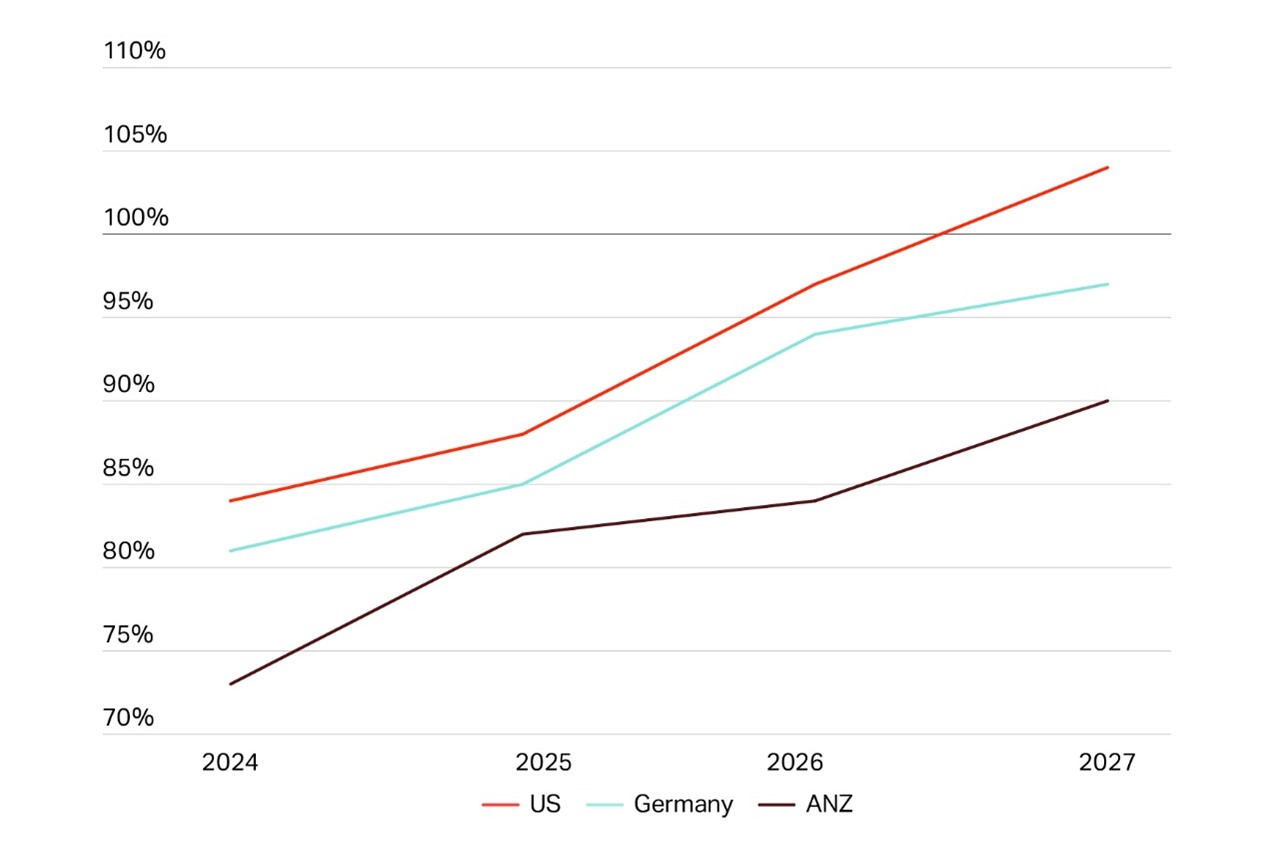

Drawing on proprietary insights across the US, Europe, the UK and Australia and New Zealand (ANZ), the report finds common structural trends, including persistent cyber threats, rising exposures and early signs of margin compression. DUAL’s analysis indicates that combined ratios are already deteriorating and could approach unprofitable levels in some markets by 2027 if current trends persist.

Australia & New Zealand

Continued softening, with pricing falling in most segments, driven by strong competition and new capacity, though margin pressure is beginning to build.Europe

Still in a softening phase, but margins are tightening and a pricing floor is expected to emerge by 2027.United States

Transitioning from a period of softening and approaching stabilisation, with pricing flattening and profitability under pressure. The market-wide combined ratio is projected to exceed 100% by 2027, based on current trajectories.United Kingdom

Late-stage softening, with slowing rate reductions and increasing signs of stabilisation.

Figure 2: Projected combined ratios in US, Europe and ANZ up to 2027

Source: DUAL, NAIC, GDV, APRA

Margins will come under pressure for some carriers if market softening persists. Two paths now lie ahead. The first leads to gradual price stabilisation over the next 12 months, supporting a sustainable and more resilient market. The second sees existing soft conditions extend into this year and next, increasing the risk of a more severe correction.

It is in clients’ interests that the market delivers the former. Underwriting expertise, portfolio resilience and long-standing relationships will determine which carriers are best positioned to navigate the next phase. Those with a proven ability to deliver consistent performance through different pricing environments will be better placed to support clients in a more complex risk environment.

Our analysis shows that underlying pressures are building. As the market moves towards a more disciplined phase, sustaining long-term capacity and pricing adequacy will be essential not only for insurers, but for the broader relevance of insurance as a mechanism for risk transfer.